The first half of 2022 has been a pretty humbling experience for most investors. A collection of factors has combined to send all major investment benchmarks materially lower. Specifically, in the second quarter, U.S. equities suffered the biggest decline falling by 13.35%, followed closely by Canadian equities which sank by 13.19% and international equities which lost 11.71%. Bonds, which have been suffering for longer, fell by a more modest 5.66%. All of this happened, while at the same time, food and gasoline costs have skyrocketed. It doesn’t seem fair!

For those looking for a little sunshine and optimism, here it is: it won’t last! We can’t predict when things will turn around, but history shows an unblemished track record of markets recovering (or things returning to “normal”) and we have no reason to believe things are any different this time around. For what it’s worth, we believe that inflation poses the greatest threat to markets recovering. Until the data shows that inflation is indisputably headed back to more normal levels, volatile and potentially negative markets could persist. For those fearing a recession and the impact that will have on the markets we suggest a few things:

- A recession is the consequence of the problem, not the problem itself – inflation is the problem.

- A recession has already been priced into market levels. Markets are forward-looking and a decline of the magnitude we have witnessed this year indicates dire economic data should be forthcoming. At some point, markets will begin pricing in the subsequent economic recovery before it happens – so don’t risk missing it!.

- Stop listening to anyone who is predicting a recession, or conversely, that there will be no recession. Short-term predictions have no value and only serve as a distraction from keeping investors focused on the long term.

To provide a bit more context on that last point, the current price of a barrel of oil is close to $100 USD. Goldman Sachs is predicting that oil will reach $140 while Citi is warning prices could drop to $65. Similarly, Morgan Stanley is predicting a US recession, while the International Monetary Fund (IMF) is not predicting a US recession. All four sources are widely followed globally, but time will prove at least two of these predictions to be 100% wrong. What will happen in practice, however, is that as the firms realize their predictions will be wrong, they will update or revise their prediction so that they no longer appear to have been wrong and offer up another useless forecast. Prediction is an art, not a science – don’t fall for it!

Since our early days back to the beginning of 2016, we have been nervous about the potential for rising interest rates and the impact it would have on the fixed income components of our portfolios. At the time, interest rates were near all-time lows, and our view at that time was that interest rate risk was the biggest risk in fixed income investing. Accordingly, we positioned our portfolios to be less interest rate sensitive (or lower duration) with emphasis on higher yielding corporate issues. This strategy has worked extremely well generating returns that are significantly better than the overall Canadian bond market over the past six+ years.

With the recent surge in interest rates, we finally witnessed the negative shock to the bond market that we feared may happen – it took more than 6 years, but it happened, nonetheless. Based on where interest rates have migrated to, we no longer felt the same sense of risk for interest rates to push significantly higher, at least from a longer-term perspective. With serious inflation concerns and central banks firmly into tightening modes, economic health becomes a more serious and immediate risk. In the bond world, that translates to fears regarding credit risk. Although we firmly believe in the longer-term viability of corporate profitability, the current environment would seem like an appropriate time to reduce credit risk.

During the months of May and June, we reduced holdings in high yield bonds and preferred equity (securities that have greater credit risk) in favour of higher quality corporate bonds and government bonds. The more conservative positioning should provide greater downside protection if the equity markets continue to sell off. The changes affected the majority of clients’ registered accounts including those that use our most popular portfolios: Justwealth Global High Growth and Justwealth Global Balanced Growth. A reminder that your account statements or the Activities section of your online access will show any transactions that have occurred in your account(s).

Market slumps are an inevitable part of investing, and they should not affect how you think about your investments. The same can be said of strong rallies in markets, they should also not affect how you think about your approach to investing. Yet, repeatedly over time, experienced and novice investors alike tend to get greedy when markets are going up and fearful when markets are going down. Our advice to you is simple: Don’t do that! The instant that you change your investments based on guessing the direction of future returns you are engaging in “market timing” and every credible bit of research will tell you that is not a wise investment strategy.

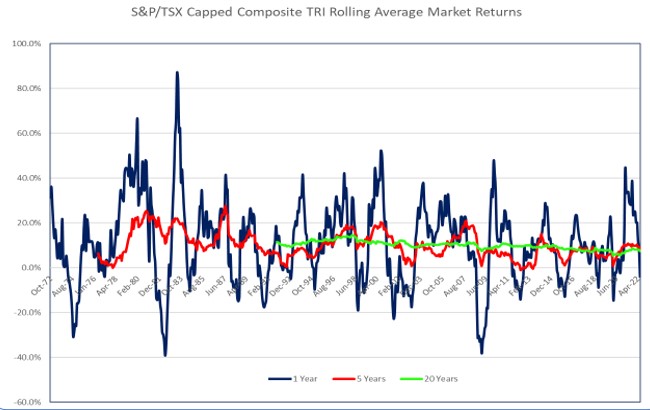

To illustrate why we consistently support long-term thinking, we present a chart that shows annual average 1-year, 5-year and 20-year returns for the S&P/TSX Capped Composite updated to the end of June 2022 (source: Morningstar Direct):

There are many important lessons that can be taught from this chart. Focusing first on the shorter-term 1-year numbers (blue line), you can see the unpredictable and extreme nature of the returns, and additionally, those large negative numbers tend to be quickly offset by large positive numbers. When you lengthen out the measurement period to the 5-year numbers (red line), it compresses the extremes quite dramatically and maybe once or twice the returns turn negative (modestly and briefly!) in close to 5 decades of observations. Finally, stretching the measurement out to 20 years (green line), the returns come predictably within a range of about 8-12%. An important conclusion here is that short-term pullbacks/corrections/crashes happen (quite regularly actually), but, time greatly reduces volatility, in other words, short-term events don’t matter much in the long run.

Keep in mind that this chart shows data for a single country’s equity market, so a comparable chart for well-diversified portfolios would exhibit a less volatile version of the above but yield the same conclusion.

Historically, patience has always been rewarded in investing. It may be uncomfortable at times to stay patient, but reacting to short-term market conditions is never a wise strategy in our opinion.

Stay safe and enjoy the summer!

Here is a recap of market performance as of June 30, 2022*

| Asset Class | Market Index | Quarter | 1 Year | 3 Years | 5 Years | 10 Years |

| Fixed Income | FTSE TMX Canada Universe Bond | -5.66% | -11.39% | -2.30% | 0.18% | 1.72% |

| Canadian Equity | S&P/TSX Capped Composite | -13.19 | -3.87 | 7.97 | 7.62 | 8.18 |

| U.S. Equity | S&P 500 ($Cdn) | -13.35 | -6.89 | 10.12 | 11.16 | 15.65 |

| Int’l Equity | MSCI EAFE ($Cdn) | -11.71 | -14.34 | 0.64 | 2.06 | 7.91 |

* Source: Morningstar Direct. Performance annualized for periods greater than 1 year.

Comments are closed.